Soubor:Securitization Market Activity.png

{kind=link}

{kind=link}

{kind=link}

Původní soubor (960 × 720 pixelů, velikost souboru: 79 KB, MIME typ: image/png)

| Tento soubor pochází z Wikimedia Commons. Níže jsou zobrazeny informace, které obsahuje jeho tamější stránka s popisem souboru. |

{kind=link}

Popis

|

K tomuto obrázku existuje vektorová verze (v SVG). Pokud je lepší, používejte raději tu.

File:Securitization Market Activity.png → File:Securitization Market Activity.svg

Podrobnější informace o vektorové grafice najdete na stránce Commons:Transition to SVG. Také si můžete přečíst informace o podpoře formátu SVG v MediaWiki. |

|

| Popis |

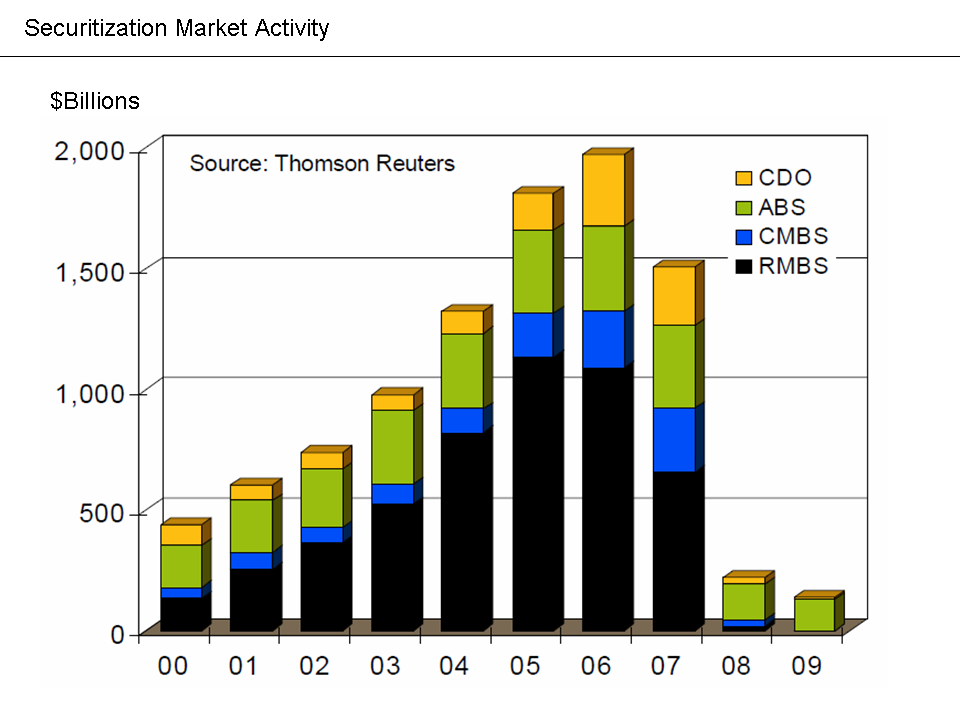

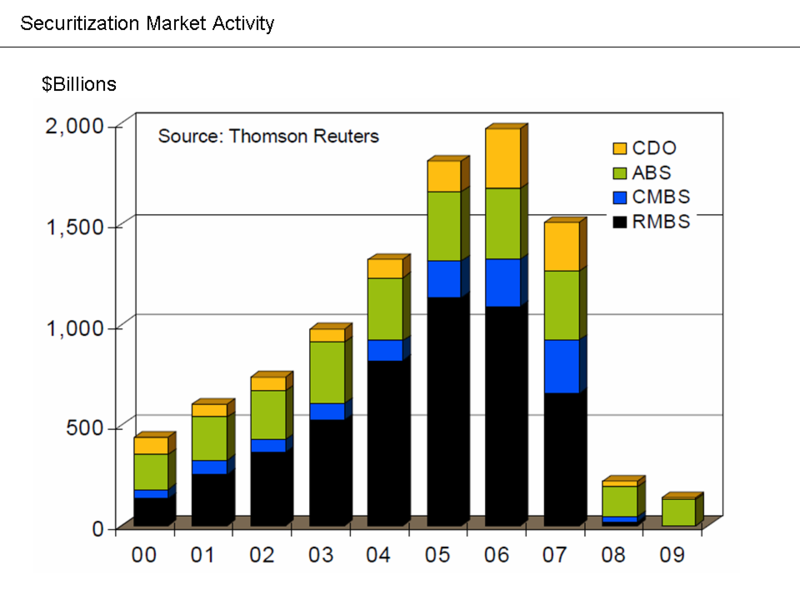

English: Image from Economist Mark Zandi's FCIC Testimony

ExplanationFrom Economist Mark Zandi's January 2010 testimony to the Financial Crisis Inquiry Commission: "The securitization markets also remain impaired, as investors anticipate more loan losses. Investors are also uncertain about coming legal and accounting rule changes and regulatory reforms. Private bond issuance of residential and commercial mortgage-backed securities, asset-backed securities, and CDOs peaked in 2006 at close to $2 trillion...In 2009, private issuance was less than $150 billion, and almost all of it was asset-backed issuance supported by the Federal Reserve's TALF program to aid credit card, auto and small-business lenders. Issuance of residential and commercial mortgage-backed securities and CDOs remains dormant."[1] Banks and other financial institutions packaged various types of loans (including mortgages) into securities and sold them to global investors. This is called securitization. In exchange for purchasing the investment, the investor receives a right to the cash flows from the underlying loans specified for the security. The chart shows how this financing source dried-up, meaning that non-prime mortgages and other types of loans could not be originated and sold to investors. |

| Zdroj | http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |

| Autor | Farcaster (talk) 04:36, 10 October 2010 (UTC) |

Licence

Toto dílo je ve Spojených státech volným dílem, protože jde o dílo úřadů americké federální vlády podle ustanovení Hlavy 17, Kapitoly 1, Sekce 105 amerického právního řádu. Viz Autorské právo.

Upozornění: uvedené se vztahuje pouze na díla úřadů federální vlády, nikoliv na úřady jednotlivých států, okresů, či nižších územně správních jednotek.

|

| |

| Bylo zjištěno, že u tohoto souboru nejsou známa žádná omezení daná autorským právem a právy s ním souvisejícími. | ||

Původní historie souboru

{kind=link}

- 2010-10-10 04:36 Farcaster 960×720× (81241 bytes) {{Information |Description = Image from Economist Mark Zandi's FCIC Testimony |Source = http://www.fcic.gov/hearings/pdfs/2010-0113-Zandi.pdf |Date = ~~~~~ |Author = ~~~~ |Permission = |other_versions = }}

Historie souboru

Kliknutím na datum a čas se zobrazí tehdejší verze souboru.

| Datum a čas | Náhled | Rozměry | Uživatel | Komentář | |

|---|---|---|---|---|---|

| současná | 14. 10. 2010, 03:07 | | 960 × 720 (79 KB) | Hideokun | {{Information |Description={{en|Image from Economist Mark Zandi's FCIC Testimony<br/> == Explanation == From Economist Mark Zandi's January 2010 testimony to the en:Financial Crisis Inquiry Commission: "The securitization markets also remain impai |

Využití souboru

Tento soubor používá následující stránka:

Globální využití souboru

Tento soubor využívají následující wiki:

- Využití na en.wikipedia.org

- Využití na fa.wikipedia.org

- Využití na hy.wikipedia.org

- Využití na it.wikipedia.org

- Využití na ja.wikipedia.org

- Využití na vi.wikipedia.org

- Využití na zh.wikipedia.org

{kind=link}